Life in the Tranches: Understanding CDOs and Risk Waterfalls

Learn how CDO tranching splits credit risk into Senior, Mezzanine, and Equity layers — with a step-by-step Python waterfall simulation.

Few financial products capture the imagination and confusion of investors quite like Collateralized Debt Obligations (CDOs). Born of the desire to turn illiquid debt into tradable securities, CDOs bundle cash flows and slice them into layers of risk and reward. This “tranching” process doesn’t just redistribute exposure; it fundamentally changes how investors think about credit, yield, and safety.

At their core, CDOs are all about tranching: taking a pool of underlying loans or bonds and splitting the cash flows into different paths. Each path has its own payment priority; senior tranches are at the top, protected from defaults by junior tranches at the bottom. These junior tranches might be the first to absorb any defaults, but they will also return eye-watering returns. The structure of CDOs allows the same pool of bonds/loans to serve many different investors willing to take different levels of risk.

In this post, we’ll see how a CDO is built from different layers, how collateral is assembled, how tranching is done, and why a simple change in structure can make the same assets appear much safer or riskier. This post will be an introduction to living life in the tranches.

Collateralized Debt Obligations

There are investors who like to take a lot of risk in exchange for the chance of a high return, and there are investors who might not be as willing to take that same level of risk. A pension fund might not be willing to take a high risk and will settle for a lower return and coupon. Other investors seeking higher returns might be willing to take greater risk. Companies can use CDOs to meet this specific demand ratio. Let’s explore a simple example to see how this would work.

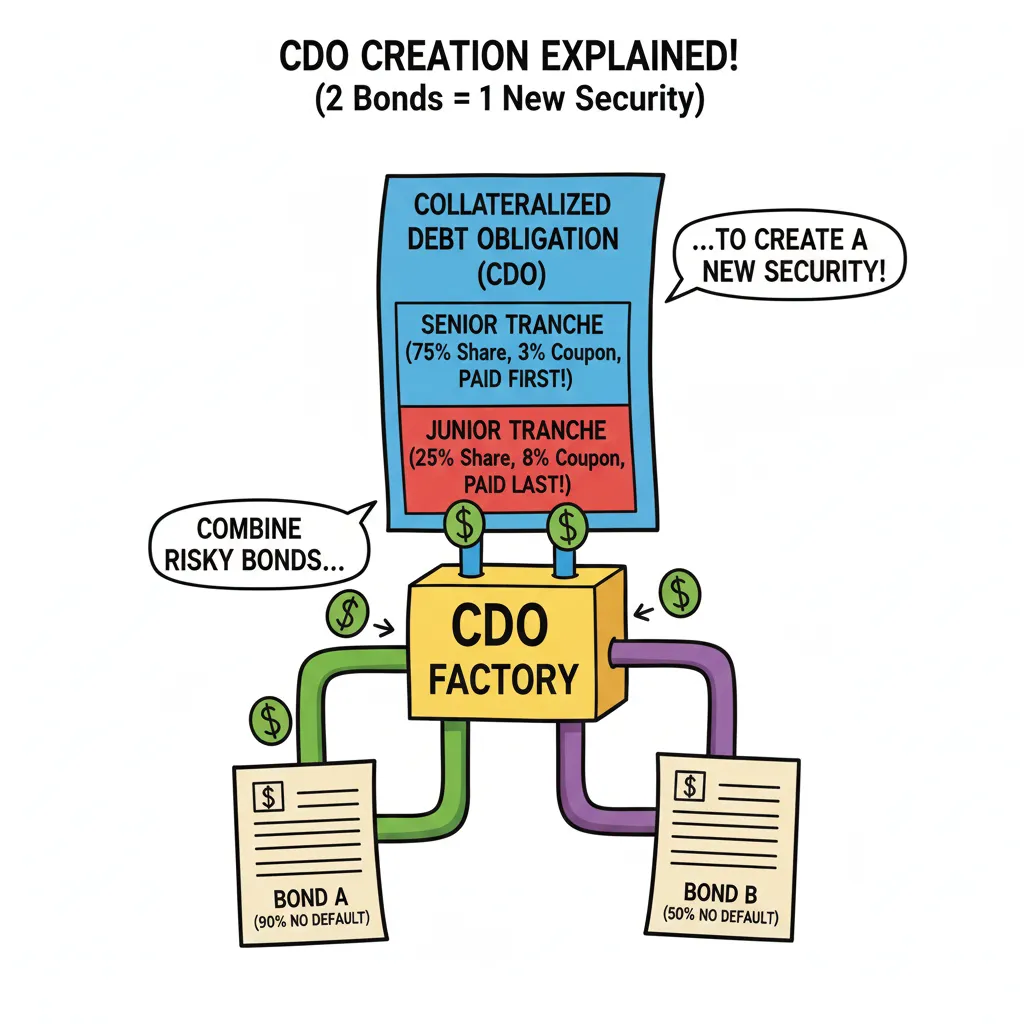

Assume we have two very simple bonds that at time cost . At time , they will either repay with probability , or they will repay with probability . Assume these two bonds have an independent chance of defaulting. In this situation, we have a pension fund that is legally prohibited from taking on more than a certain level of risk. The two bonds we have are currently too risky for the pension fund to purchase. How can we issue a new financial bond so the pension fund can make this investment?

We do this by buying the two bonds and putting them into a legal structure that protects them from the outside world. The cash flow arising from this new structure is divided between investors in a special way. We create two new fixed-income securities: a junior and senior tranche. These junior and senior tranches refer to the order in which investors are paid out in case of a default. The junior tranche will only get paid after the senior tranche has been paid. If our CDO is split evenly between junior and senior tranches, what would happen if one of the bonds in the CDO defaulted? Well, the senior tranche would be paid with the principal supplied by the bond that did not default. However, the junior tranche would lose its principal, as there is no further cash flow available. Only in the unlikely event that all bonds in our CDO default would the senior tranche not get back its principal.

To offset this risk for junior tranche holders, they will receive a higher coupon. So, if neither of the bonds in our simple CDO defaults, both the junior and senior tranches will receive their principal, and on top of that principal, the junior tranche will receive a higher coupon. We need to find a coupon high enough so that investors in both tranches are willing to buy the bond.

Let’s assume that the junior tranches have a probability p of defaulting; therefore, the senior tranche has a probability of defaulting. In the event of a bond default, the recovery rate is . Given this, the minimum platatable coupon rate we need to pay the senior tranche is:

The interest remaining to pay the junior tranche can be found using the formula:

Because it is highly unlikely that both bonds in our CDO default, the junior tranche actually has a small recovery rate if only one bond defaults. The bond that did not default will still pay its coupon, allowing for some recovery rate. The recovery rate R_2 for the junior tranche in this case can be calculated as:

CDO Simulations

Having a CDO consisting of just two bonds is a good example to get a clear understanding of how they work. However, this kind of CDO is not very realistic in the actual world. Luckily, even CDOs composed of many different bonds share the same cash flow principles as the small CDO we have discussed so far.

Our new CDO will consist of three tranches: A, B, and C. Tranche A is the senior tranche, and tranche C is the junior tranche. In this simulation, we do not consider the bonds’ ability to pay a fair coupon rate, as we did before. All the parameters for this simulation are listed in the table below.

| 3% | |

|---|---|

| €1000 | |

| 5% | |

| 0% | |

| 8% | |

| 12% |

The thicknesses of tranches A, B and C in our CDO are shown in the table below. Tranche A and B will be the biggest tranches, and our junior tranche C will simply receive whatever is left after tranches A and B have been paid.

| Tranche | Tickeness | Coupon | Coupon % |

|---|---|---|---|

| Tranche A | 70% | 3% | |

| Tranche B | 20% | 8% | |

| Tranche C | 10% | 15% |

In the previous post about default risk, we wrote a small script to simulate the result of a simple bond structure. Let’s adjust this script a bit so we can simulate a more complicated CDO structure with different tranches, ticknesses, and coupons.

import random

import math

from typing import List

class BondPricing:

def __init__(

self,

trials: int,

num_loans: int,

loan_principal: float,

interest_rate: float,

default_prob: float,

tranche_thickness: List[float],

tranche_coupons: List[float],

tranche_min_recovery: List[float],

):

self.trials = trials

self.num_loans = num_loans

self.X = loan_principal

self.r = interest_rate

self.p = default_prob

self.tranche_thickness = tranche_thickness

self.tranche_coupons = tranche_coupons

self.tranche_min_recovery = tranche_min_recovery

self.validate_tranches()

def validate_tranches(self) -> None:

if not (

len(self.tranche_thickness)

== len(self.tranche_coupons)

== len(self.tranche_min_recovery)

):

raise RuntimeError("All tranche vectors must have identical sizes.")

total = 0.0

for t in self.tranche_thickness:

if t <= 0.0:

raise RuntimeError("Tranche thickness must be positive.")

total += t

if abs(total - 1.0) > 1e-6:

raise RuntimeError("Tranche thickness must sum to 1.0")

for rr in self.tranche_min_recovery:

if rr < 0.0 or rr > 1.0:

raise RuntimeError(

"Tranche minimum recovery must be between 0 and 1"

)

def get_portfolio_principal(self) -> float:

return self.num_loans * self.X

def get_num_tranches(self) -> int:

return len(self.tranche_thickness)

def simulate_bond_pricing(self) -> None:

n_tranches = self.get_num_tranches()

portfolio_notional = self.get_portfolio_principal()

tranche_returns = [[] for _ in range(n_tranches)]

for _ in range(self.trials):

default_count = 0

performing_count = 0

total_loss = 0.0

coupon_pool = 0.0

# Simulate loan defaults

for _ in range(self.num_loans):

is_default = random.random() < self.p

if is_default:

loan_recovery = 0.40

default_count += 1

total_loss += self.X * (1.0 - loan_recovery)

else:

performing_count += 1

coupon_pool += self.X * self.r

# Initialize tranches

tranche_init = [

t * portfolio_notional for t in self.tranche_thickness

]

tranche_remaining = tranche_init.copy()

remaining_loss = total_loss

# Loss waterfall (junior → senior)

for i in range(n_tranches):

if remaining_loss <= 1e-12:

break

absorbed = min(remaining_loss, tranche_remaining[i])

tranche_remaining[i] -= absorbed

remaining_loss -= absorbed

# Coupon waterfall (senior → junior)

tranche_coupons_paid = [0.0] * n_tranches

for i in reversed(range(n_tranches)):

if tranche_remaining[i] > 1e-12:

due = tranche_init[i] * self.tranche_coupons[i]

paid = min(coupon_pool, due)

tranche_coupons_paid[i] = paid

coupon_pool -= paid

# Compute returns

for i in range(n_tranches):

end_value = tranche_remaining[i] + tranche_coupons_paid[i]

if tranche_init[i] > 0.0:

ret = (end_value - tranche_init[i]) / tranche_init[i]

else:

ret = 0.0

tranche_returns[i].append(ret)

# Output results

print("\n================= TRANCHE RESULTS =================")

for i in range(n_tranches):

rets = tranche_returns[i]

mean = sum(rets) / self.trials

best = max(rets)

worst = min(rets)

variance = sum((r - mean) ** 2 for r in rets) / self.trials

stddev = math.sqrt(variance)

print(f"\n--- Tranche {i + 1} ---")

print(f"Thickness: {self.tranche_thickness[i] * 100:.2f}%")

print(f"Coupon: {self.tranche_coupons[i] * 100:.2f}%")

print(f"Min Recov: {self.tranche_min_recovery[i] * 100:.2f}%")

print(f"Avg Return: {mean * 100:.2f}%")

print(f"Best Case: {best * 100:.2f}%")

print(f"Worst Case: {worst * 100:.2f}%")

print(f"Std Dev: {stddev * 100:.2f}%")

print("===================================================")

Compared to the previous script, we added some extra variables and methods to this header. We added methods to validate the tranches’ configuration, to calculate the total principal of the CDO portfolio, and to count the number of tranches in the CDO.

The simulation demonstrates how tranche design fundamentally shapes the risk-return profile of a CDO. Even though the underlying loan pool is homogeneous and relatively simple. The distribution of losses and coupons across tranches produces dramatically different outcomes.

To better understand these outcomes, we can analyze each tranche’s performance using a Sharpe-like ratio, which provides insight into how returns compare to volatility. The junior tranche absorbs losses first and carries substantial risk, exhibiting high volatility with outcomes ranging from full principal loss to full coupon payment. Its average negative return suggests that it effectively sells insurance against portfolio defaults, highlighting a low risk-adjusted return.

The mezzanine tranche offers a more balanced profile, with lower volatility than the junior tranche. It presents a smaller coupon and a slightly lower exposure to losses, meaning it would require significant CDO-wide losses before it incurs losses. As such, its risk-adjusted return is more stable than that of the junior tranche.

Finally, the senior tranche resembles a nearly risk-free instrument, with losses rarely affecting it. Its consistent returns, even in worst-case scenarios, reflect a high risk-adjusted return, demonstrating the stability that appeals to conservative investors. By relating returns to volatility in this manner, investors can make more informed decisions when assessing the appeal of each tranche. This type of risk-adjusted analysis is highly relevant when evaluating CDO investments.

⚠️ Financial Education Disclaimer

This post discusses Collateralized Debt Obligations (CDOs), which are highly complex financial instruments. The models and Python simulations provided are for educational purposes only.

- Correlation Risk: The provided simulation assumes a simplified default probability. In reality, CDOs are highly sensitive to “Default Correlation”—the risk that many loans fail at once due to systemic economic shifts.

- Model Limitations: A simple Monte Carlo simulation cannot account for liquidity risks, credit rating migrations, or the “tail risk” associated with real-world housing or corporate debt markets.

- Historical Context: Investors should be aware that structural flaws in CDO modeling and rating contributed significantly to the 2008 Global Financial Crisis.

- Professional Advice Required: Structured products should only be traded or invested in by institutional or sophisticated investors. Consult a licensed financial professional before engaging with these instruments.